A Mad Fientist reader named Brian reached out to me and said that he increased his savings rate by utilizing some of the tax-avoidance strategies I write about here.

Not only did these strategies help him to save more, they also allowed him to take advantage of other tax benefits that he hadn’t previously been eligible for (which then reduced his costs even more)!

He asked if I’d be interested in a case study (with his actual numbers) and I said yes!

Take it away, Brian…

If you’re frugal and willing to learn a little bit about the nuances in the tax code, you can save a massive percentage of your earnings every year.

This can be done by stacking the benefits of tax-advantaged savings.

By maximizing tax-deferred accounts first, a moderate income earner drives down their adjusted gross income (AGI). This in turn, may drastically reduce or even eliminate some of their largest yearly expenses.

How to Reduce Your Adjusted Gross Income (AGI)

Reduce your AGI by contributing to the following accounts:

- Traditional 401k

- Traditional IRA

- Health Savings Account (HSA)

Benefits of a Lower AGI

Lowering your AGI opens the possibility for:

- Becoming eligible for premium tax credits for health insurance

- Reducing or eliminating student loan payments

- Claiming additional tax credits (retirement savings credit, etc.)

- Receiving stimulus payments or other one-time benefits

My Numbers

Here is the strategy I’ve implemented for the past few years…

My total income was $58,070 for tax year 2020.

After contributing the maximum of $19,500 to my Traditional 401K and $6,000 to my Traditional IRA, my AGI was lowered to $32,570.

Now, here’s the interesting part. I purchased my health insurance through the ACA marketplace*. I’m fortunate to have good health, so I always select a high deductible health plan (HDHP) that is HSA compatible. I then maximized the HSA contribution ($3,550 for tax year 2020). This resulted in a health plan with a monthly premium of about $54 after the ACA Tax Credit (thanks to my lower AGI).

I’ve done this for the past few years and it’s been a great way to obtain low-cost health insurance while building up what the Mad Fientist calls the Ultimate Retirement Account.

Another bonus to accessing an HSA is that you can use it to lower your AGI even further. My already significantly-lowered AGI of $32,500 then became $29,020, which allowed me to claim the Retirement Savings Contributions Credit** for $200 (which in turn lowered my final tax liability).

The end result was a federal tax bill of about $1,607. Not bad!

Additionally, I live in a state where most of my income would fall in the 9% tax rate, so reducing state tax liability is another perk to consider when reducing your AGI. That being said, I’ve excluded state taxes for the sake of simplicity.

Here is an annual breakdown of my numbers compared to a lower savings rate of 5%:

| Low Saver | High Saver | |

|---|---|---|

| Income | $58,070 | $58,070 |

| 401k Contribution | $2,904 | $19,500 |

| Traditional IRA | $0 | $6,000 |

| HSA | $0 | $3,550 |

| AGI | $55,166 | $29,020 |

And here are my annual costs:

| Low Saver | High Saver | |

|---|---|---|

| Health Plan | $5,408 | $648 |

| FICA Taxes | $4,365 | $4,365 |

| Federal Taxes | $4,944 | $1,607 |

| Cost Savings | $8,097 |

New Tax Changes – ARPA

Due to the American Rescue Plan Act (ARPA passed in March 2021), participants in the ACA marketplace receive additional subsidies on the same level of income for 2021 and 2022.

Also, higher income earners may now qualify for a subsidy. This opens the door to qualify for low- or no-cost health insurance even with a slighter higher AGI. I’m currently exploring the option of keeping my monthly premium the same, while converting some of my traditional IRA to a Roth IRA, which would not have been possible prior to the ARPA.

AGI and Student Loan Payments

For those with federal student loans, reducing your AGI can also significantly reduce or eliminate student loan payments, depending on your repayment plan.

I was fortunate to graduate with a very modest amount of debt, so I was able to pay the balance off in a couple of years. However, I’ve known others with large debts relative to their income that used this strategy to bring their monthly student loan payments down to $0 while building up healthy retirement accounts. Some have even combined this with Public Service Loan Forgiveness to wipe out their loans completely after 10 years!

Conclusion

In summary, it is possible to save a massive amount for retirement while minimizing or eliminating other expenses. I encourage your readers to explore how they can stack the benefits available to them in order to save more for retirement while living a great life during their working years.

I look forward to any responses in the comments on other tax savvy ways to save.

Cheers!

* My employer only offers a low deductible health insurance plan, which normally would exclude me from taking part in the ACA marketplace. However, the premiums are higher than the minimum value standard which allows me to opt into an ACA plan.

** See Retirement Savings Contribution Credit qualification tables in the links below.

Resources

- Affordable Coverage definition for ACA

- Retirement Savings Contributions Credit qualification tables

- Here is a great subsidy calculator from the Kaiser Family Foundation. It’s been updated to reflect the most recent changes to ACA subsidies.

Thanks, looking forward to this journey.

Thanks for this, actual numbers really drive home the advantages! I also prioritize my HSA, have done so since I stumbled upon the Mad Fientist’s original post. Brian, my question is about your annual costs breakdown. You have FICA taxes as the same between high- and low- savers. But HSA contributions reduce FICA tax burden, too… right? So the low-savers FICA numbers should be even less?

HSA contributions reduce the FICA tax burden if they are made via payroll deduction, not if you contribute to an HSA directly.

Yep this is correct. I had to ask my employer to set this up for me.

Every little bit helps

Yeah, I wish my employer offered a HDHP with an HSA option so I could save of FICA taxes, but we all have to work with what we’ve got :)

Thanks for the clarification! My deductions are through payroll, too.

Good piece, Brian! Seems you’re making the most of what you have.

How early are you planning to become FI with annual savings of 30k? Do you plan to have a family as well?

How do you access 401K when retired?

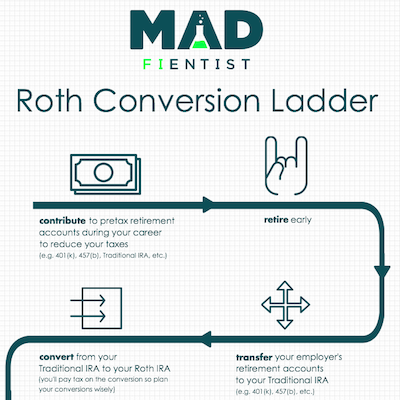

One way is to do Roth conversions (after leaving the workplace & earning income). Essentially you can control your AGI while doing this and can have a double benefit for the ACA subsidies & controlling your tax on the conversions. Then after doing this for 5 years, you can withdraw your initial conversion (not growth) from year 1.

Lots of reading on this, but it’s not guaranteed to be available forever.

I meant, how do you contribute to a 401k when retired?

You don’t. Your 401k is funded by your employer withholding some of your paycheck. When you retire, you typically roll the 401k over into an IRA. Then all of the usual IRA rules apply. If it was a ROTH 401k, then it rolls to a ROTH IRA.

Brian, since you are in such a low tax bracket, wouldn’t it make sense to be putting your 401k into a ROTH 401k instead? You’ll likely not be paying such a low tax rate in the future.

Madfientist has been retired for several years, how is he able to contribute to a 401k?

I believe he doesn’t draw down on his federal retirement accounts yet. Self-employed folks can set up a SEP-401k and a SEP-IRA. There’s a good guide to it here: https://www.irs.gov/retirement-plans/retirement-plans-for-self-employed-people

Sheltering income via these commonly available tools is a great start, one that’s good for any income level as it removes exposure at the top of the bracket.

However a better strategy is to find ways to make more income, possibly through a business. Take at a look at Todd Tresidder’s work on leverage.

Would love to see more of these case studies with real numbers! From high-earning individuals… from families with higher healthcare costs… from self-employed individuals… So very helpful.

I loved that you took all of these great strategies and increased your investing. The title of the article also implies you did this without decreasing spending. Other than the tax savings, you didn’t really touch on that aspect in your review. I would love to hear more about that piece as many will say they would like to save more but simply can’t afford to invest another dime. Did you find ways to reduce your spending as well? Personally I have always found that when you increase your savings / investing fewer dollars flowed into your checking account. We always spent less but never really felt like it or even noticed it. I’d love to hear more about your experiences on the spending side of the equation.

Hey Bruce, see my reply to Wes below.

The math is off. In the body of the article it mentions Monthly Healthcare premium of $54. In the tables it’s listed annually at $54, a difference of $594, this also doesn’t include anything out of pocket paid towards a deductible.

Good catch, thanks! Table has been updated.

Thank you, Brian for sharing your experience and your methods of savings along with the numbers and the breakdown. Examples like this help folks understand that not only is the hope of financial independence real but that it is possible as well.

Thanks once again!

Thank you for this wonderful info.

I like the idea of being able to control my income and therefore income taxes through how much I withdraw from my 401k/traditional IRA. This is because taxes are based on income of course.

However, I want to remind people that these taxes not paid this year are DEFERRED. They need to be paid later and hopefully at a lower rate.

I always love a good case study! Thanks for sharing.

It would be helpful to show the net income differences between the low saver and high saver, not just the savings amount and savings rate. The person who is close to living paycheck-to-paycheck would greatly benefit from seeing that (as I expect) the gap in the two net incomes is not too big of a spread to overcome.

Thanks a lot for your comment, Wes. It made me realize I had left a big piece of information out of the post (Net Income) when I copied it over from the PDF Brian sent me. And looking at the Net Income, I realized the savings rate difference isn’t actually as great (since the Low Earner could invest the additional net income into a taxable account or other savings account).

To rectify this, I’ve renamed the post (and url) to focus on the main point of this guest post…stacking tax advantages to obtain even more tax benefits.

Big apologies to everyone for the misleading initial title. This is what I get for trying to publish a post when I’m in Spain :/

Thank you for this core advice! And thank you for sharing this reader case study! I was able to implement the maximum retirement savings (or nearly) on a similar income about 2 years ago. It has dramatically increased my savings and net worth. I may be moving to a job with access to an HSA option, and appreciate the vantage point on those.

A couple of questions/ comments.

1) For those excited by the title (I was), it seems a little misleading. The 10x is right there in the difference between the High and Low Saver sample numbers – saving $2,900 vs. $29,050.

I think for folks new to FI, or new to these specific methods, this may seem discouraging or disingenuous. I was able to do this too and it wasn’t especially hard (given my cost of living, and having no: car payment, mortgage, dependents, or any major surprise expenses relative to my net worth).

It doesn’t make as snappy a title, but it’s more accurate to say that “Uncle Sam can match you up to 30% – if you increase your retirement savings*! ” (*If you have access to both a 401k/ 403b and HSA through your employer.)

The savings/contributions are the biggest component of the gains in the short-term. At some points I would feel discouraged about this myself. The way I started thinking about it was that by maxing out my retirement accounts and lowering my AGI, I was getting a guaranteed “return” from the IRS. I saw it as investing a “gain” (from tax avoidance) in my retirement account. (Though I was often making catch-up contributions to my Traditional IRA by tax day out of my cash accounts and getting a tax refund later for a portion of that.)

2) This advice has definitely worked for me and I so appreciate it. But it’s far from one-size-fits all. This is a longer conversation/ challenge for more than one post or FIRE blogger/ educator/ role model.

Does anyone know about good “starter” FIRE resources that might apply to friends with crappy jobs?

Are there FIRE resources you’ve shared with friends who: … have low incomes and vulnerable finances? … are nearing retirement age who feel confused and hopeless? But most of what I have found is pitched to people with access to even more income & resources than I currently have.

I so appreciate your past post/s detailing the methods & math on the enormous benefits of maxing out retirement accounts (and using HSAs when you have them). In part, they simply encouraged me to assume I was eligible to save in both my 401k and Traditional IRA. I was seeing instructions (in Turbo Tax maybe?) that gave me the appearance that this wouldn’t be allowed, or that it wouldn’t lower my tax liability. Your post lit a fire under me to keep looking into the IRA guidelines to assure myself I was eligible. It also spurred me to check and see what kind of health savings plan I had.

3) Several things in the expenses table confuse me. It seems to show the monthly healthcare costs vs. annual ones in the High Saver column ($54*12 = $648). You may think all the readers or FI types all have strong mental math skills. (I’m embarrassed to say, I regularly lose powers of ten in my own mental calculations!) Seeing it all laid out is so helpful. Also, the savings total at the bottom of the High Saver column isn’t quite transparent. So it’s $5,408 – $648 = $4760 lower expenses for healthcare premiums. And $4,944 – $1,607 = $3337 less in federal taxes. Summing those lower expenses $4760 + $3337 = $8097 But the total lists $8,691? Building on others’ comments, is the difference the lower FICA taxes from making HSA contributions via payroll deductions?

1) Yes, see my comment to Wes and big apologies for the title. Although it was accurate (Brian is saving 10x more than he was before), it didn’t capture the full picture.

2) Not sure exactly what you’re looking for here but maybe someone in the comments will have a suggestion?

3) Correct, the monthly number was in the table (instead of the annualized value) but the table has been corrected!

As per number 2, I’ve had success with starting friends off with Ramsey’s Total Money Makeover. I’m not a huge Ramsey fan, but I’ve found his stuff is a decent gateway drug for more standard FI stuff. I could go on for awhile about my theory of the efficacy of influencing people when the rest of our culture wants them to go the other way, but my N is like 7 so I don’t think I can draw conclusions from that.

Anyways, IF they latch on to Ramsey, and get through his “baby steps”, then I’ll hit them with a one two of JL Collins and Mr Money Mustache. JL will provide plenty of good material on how to invest, and MMM provides motivation after they’ve already been primed by Ramsey.

If they’re still looking for more at that point, I point them to this blog and Early Retirement Now. You really got to be all in to get stoked about Roth conversions and glidepaths. Save the best for last!

Good luck in your efforts, just remember that old chestnut about leading a horse to water. Can’t remember how it goes exactly, and I refuse to google it, but basically it’s hard to get people to do stuff they don’t want to do even it’s in their best interest.

Finally, it’s probably helps most just to provide a good example. At work I never work overtime, and am always taking time off to do fun stuff. When people ask about it, only then do I nudge them down the rabbit hole.

I feel like the title was kinda clickbait but it’s good info. I’m already doing all of these things however.

I can say that they work however at least? Last year my total income was around $44k and my ACA ended up being $28.30/ for a bronze plan with HSA. *ALTHOUGH* it actually is now less than that- IBX just sent me a check for $320 bc apparently they get in trouble if they don’t spend at least 80% of their premiums on actual healthcare right now. So it looks like my healthcare was $20 for the ENTIRE YEAR? This is nuts.

I’ve never had a 401k match since I’ve mostly been self employed (or otherwise no benefits) but I opened up a solo401k which is an even better choice. I was happy to see an example with a smaller (tho! still substantial) income for once. Since I learned about retirement/investing in general, and FIRE in particular 2 years ago, I’ve been doing what the author suggested on my income of $30-50k. Maxed HSA, solo401k, and IRA.

Once you have these things down, maximizing bank/CC bonuses, getting good savings accounts (I have a mix of HYSA, and crypto USDC accounts paying out currently 9%) and regular investing apart from your “retirement” accounts (I put a small amount weekly into a brokerage and BTC) and that adds up really fast. Apart from student loans (which will be forgiven- I am saving for the tax bomb, and have paid $0 to date bc my income is so low), I’ve gone from $0 to over $100k worth in exactly 2 years to the day. Super close to baristaFIRE since my COL is very low, but I’ll hang on a bit longer to my main profession to pad things and wait for the house to be paid off (2-3 years).

Sorry about the title, Dizzy (see my reply to Wes above).

That’s crazy/great your healthcare is so cheap and big congrats on your FI progress!

9%!!? That’s awesome. Can you please provide details on how you’re doing that?

Great job on your progress, you’re killing it.

Thanks for this! I love reading real-life case studies! I would like to see how the extra savings affected your take-home pay. I would like to contribute more for the tax savings, but would like to see how it would affect my own take-home pay also. Any calculators out there for this?

A great exercise I’ve done in previous years is build my own tax calculator in a spreadsheet. So I go through my last 1040, look at all the fields with values, figure out how they all fit together (e.g. this field minus this field equals this field), and build a calculator that works it all out (so that I can then tweak values to see how it impacts my final tax bill). It’s time consuming and sometimes frustrating but once you’ve done it, you know how everything interacts and you know which levers to pull when you need to lower your AGI, MAGI, etc.

Great article but not helpful to some some one who is a high income earner a couple together making over $600k the 19.5K max contribution per person is a drop in the bucket and still does not bring down AGI below $400K even with the HSA and traditional IRA contributions. No matter what federal Taxes are astronomical at this income range, i would love to see more articles that reflect help for those in these income ranges to reduce tax burden. especially in my case where student loans curtail ones ability to save.

For the high income crowd I recommend the White Coat Investor blog/podcast. It focuses on the finances of people who make a ton of money. From what I’ve learned, unless you own your own business and can do things le a solo 401k or a cash balance deferred compensation plan, you likely don’t have many options aside from maxing out tax deferred retirement accounts, HSA, and perhaps a 529.

But don’t stress too much. 1) you earn an amazing income and 2) your effective tax rate is quite a bit lower than it would be in any other developed country. Congrats on winning the finances game.

It sounds like paying off the student loans would really help your situation. I would start there. As for reducing taxes on $400K income? Start a business or donate to charity; those are your off sets.

As mentioned, a deferred compensation plan can work really well (I can contribute up to 80% of regular pay and 100% of annual bonus). The other option I have seen mentioned is for one spouse (usually the lower earning if there is a big difference in income) to obtain the real estate professional status so that depreciation from rentals can be used to offset regular income taxes.

Fabulous, simple, numbers roadmap to clearly show and explanation what to do for one’s personal situation. Thank you! I am 55 and have been striving to convert ALL of my SEP and IRA monies into my ROTH as each tax year allows (for lowest amount to be paid) until 100% converted. All of this to be done by the time I choose to stop working, limiting my tax liabilities to whatever Social Security benefits i receive and thus helping me qualify for the lowest medical premiums through the ACA as possible.

For your example and other s with low AGIs, you may also qualify for a Savers Credit.

How are you able to max out your company 401k @ $19,500 and a traditional IRA @ $6k?… I was understanding that per the IRS you could not contribute to both plans and exceed $19,500 tax free as a total contribuiton per year.

You can contribute to both a 401k (Roth or traditional) and an IRA (Roth or traditional) so long as your income is within the limits for each. Not sure where you read you couldn’t contribute to both, but that was wrong.

I’m not sure where you heard this… 401K and IRA are different vehicles for retirement savings and the limits are independent.

Hi, I live in CA and self employed (operating small restaurant). Shopping for an affordable health insurance for myself, can you advise me with this please? I’m healthy and hardly go to see Dr. I do have a small IRA

This is great information. My wife and I file separately since she is doing Public Service Loan Forgiveness (only three years to go). Since her debt will get forgiven, the balance doesnt matter, we want to minimize her AGI to lower her monthly payment. We utilize all of these strategies here plus have her claim our child to reduce her tax burden, save for retirement and minimize tax burden.

Ryan, one thing to keep in mind is that, as far as I know, forgiven debt counts as income in the year that it is forgiven so the balance will matter from that perspective as income taxes will be due on the forgiven debt.

If you’re eligible for PSLF, the IRS does not consider that income for tax purposes.

https://studentaid.gov/help-center/answers/article/loan-amounts-forgiven-under-pslf-taxable

If you’re not on PSLF, but are eligible to have your loans discharged after the required 20 or 25 years you may not have to pay taxes on the discharged amount. The American Rescue Plan Act made federal, private and institutional student loan forgiveness tax-free through 2025.

https://studentloanhero.com/featured/owe-taxes-student-loan-forgiveness/

I’ve been doing this for years, but never could quite explain it as good as you did. One additional thing people can look into is finding out whether they can invest the HSA money, especially if they are in good health. I was able to invest my HSA money the past few years because my employer offered a plan that allowed it. And now it has really grown, increasing my net worth. My HSA is with HSA bank and I invest through TD Ameritrade. I’m up 460% in the last 3 years!!! I got lucky with one high growth/high risk investment, but even a conservative investment can make a huge difference in the long term. Definitely look into.

Great case study. Curious – why did you opt to contribute to a traditional IRA when you are eligible to contribute to a Roth IRA at your income level?

Thanks for sharing your playbook,

CD

Great question, because just looking at tax brackets the IRA would be saving only 12%. If one expected marginal tax rates on withdrawals to be higher, using a Roth IRA now would be logical.

But with the ACA and saver’s credit effects, the actual marginal tax rate savings for a traditional IRA in this case can be much higher. The actual tax rates will depend on the amount of Advance Premium Tax Credit (APTC) received, because repayment of excess APTC is not a mirror image of the Premium Tax Credit (PTC) one gets if filing without any APTC.

No really good rules of thumb available – one has to run the numbers for the specific situation to understand what the whole situation is.

I agree MDM. I may start tilting my savings more toward Roth accounts, but when considering the APTC, saver’s credit, and reduced taxes it is hard to willingly increase tax costs. I also do not expect to spend very much in retirement, so I don’t foresee needing to withdraw large taxable amounts every year. If I can withdraw close to the standard deduction, then even withdrawals from tax-deferred accounts will not be taxed. This is basically what my retired parents do and it works well for them.

Great article! We’re within months of ER and are weighing our tax options so it was timely for us. We’ve read all past articles and this one too makes good use of tax benefits. When we do our math, however, the marginal tax comparison is very close of whether to favor a low income before Medicare age to get an excellent silver 200% FPL ACA plan and then be faced with larger RMDs (in addition to a good pension and SS) which will drive up our tax rate. Or in doing more Roth conversions and give up on the great ACA subsidies so RMDs and taxes will be lower later. The later protects a surviving spouse better in case of death of the other and the former keeps more money in hand to be invested and growing. But essentially they end very close to the same average marginal tax rate. I’m also going to look at an option of higher Roth conversions until 2026 to take advantage of the very low tax rates (unless the tax law changes earlier) and then dialing the Roth conversions way back to have the lower income and good ACA subsidies for the remainder of the early years before Medicare. I know you advocate strongly to take tax breaks now but are there any cases where that isn’t the clear-cut answer both mathematically and other reasons?

“Premiums are higher than the minimum value standard”

How did you figure this out? Is it just based on 2nd cheapest silver plan?

Nice work!! I’ve been doing all these things and it’s really been making a difference!! I’ve been shocked at the actual balances in my accounts. It gives me hope I can retire early. I just wish it was happening tomorrow.

Can you talk more about the minimum value standard mentioned?

I have a question about Roth conversion ladders and social security earnings.

I have been completing Roth conversion ladders for a few years. I noticed when I signed on to the social security website my Roth conversion seems to be improving my yearly social security earnings. Is this correct?

If so, this is yet another benefit of Roth conversion ladders?

Can someone double check my figures on there own Roth conversion ladders and social security earnings?

–Don

I don’t see mention of the Qualified Business Income Deduction here. My understanding is that by making traditional 401k contributions instead of Roth, you reduce the QBI deduction you were going to get. That’s one argument for making Roth contributions. Seems to be missing from Brian’s analysis?

This post is great and so informative. I’ve been thinking about how tax-deferred benefits intersect with government benefits since I got my first real/ corporate job a few months ago and would like to add a few comments and questions:

I make 50K a year in W2 income and my husband is self-employed, which means he can deduct lots of business expenses and show very little income. We have 2 kids, so a family of 4. Our state has expanded Medicaid which covers the kids health insurance.

If I take the max 401K benefit and HSA benefit from my work (say 23K for the sake of round numbers) my AGI would be $27,000 yearly. Would my husband then be eligible for Medicaid? Or does the fact that my work offers a spousal health plan mean that he has to buy into the low premium/ high deductible option that I signed up for?

In researching this question, I’ve found out that the ACA and Medicaid benefits are based on MAGI, as is WIC (available to pregnant women and low income families with children under 5). Other government benefits, like food stamps or childcare assistance (varies by state) are based on gross income. The cutoff for many programs is 138% of the poverty limit, which my family hovers around. I’m not sure if stimulus payments are based on gross income or MAGI but my guess is adjusted. Annoyingly, many sites just ask for “income” without specifying gross or net. Does anyone know any other examples? And what about EITC?

Lots to chew on here, thanks again!

When do social security spousal benefits work to your advantage?

We would like to start claiming my wife’s social security benefits at 62, then claim spousal benefits at 65, when my payments would kick in. Since her benefits are less than half of mine at 65, I interpret the rule to mean that she could claim half my benefit, once I begin claiming mine at 65. So, we end up claiming a bit more as a couple than we could independently. Does this make sense?